CoreWeave: Unit Economics, Margin Profile, and Leverage Analysis

$CRWV

After nearly a year as a public company, many market participants still do not understand CoreWeave’s business and financial model, particularly around CapEx and use of debt. This post addresses the following questions:

What are the underlying unit economics for a 100MW GPU cluster?

Are CoreWeave’s current margins representative of its longer-term margin profile?

Why does CoreWeave use debt? Is its leverage “reckless”, posing a “ticking time bomb”?

What are the real risks to CoreWeave’s lenders, shareholders, and data center landlords?

Business Model Overview

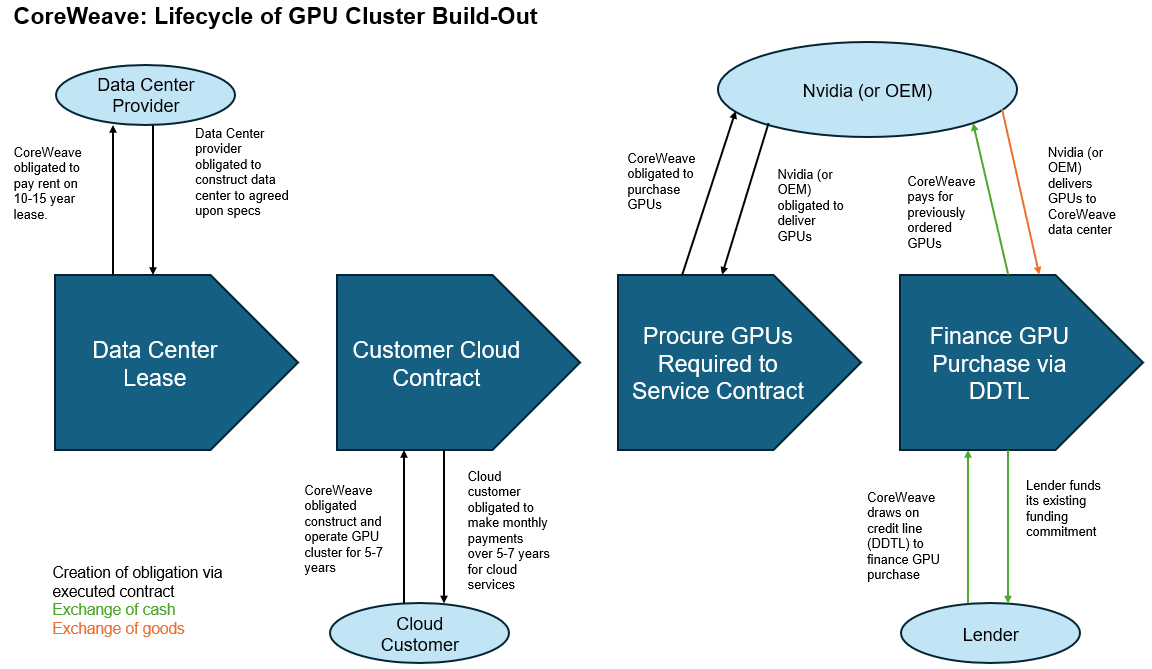

Before examining the details of a 100MW cluster-level financial model (referred to herein as the “100MW Model”), an overview of CoreWeave’s business model and the lifecycle of a customer contract is helpful. Note that the order of operations is important:

CoreWeave signs a lease with a data center co-location provider, who then builds out the data center. CoreWeave, as the tenant, provides precise specifications as to the type (i.e. liquid cooling) and configuration of the data center’s electrical and cooling equipment, which the provider procures and installs. When construction of the data center is completed, CoreWeave brings its GPUs to the data center facility to operate.

In the 100MW Model, the data center provider incurs the CapEx for the physical building shell, cooling equipment, and electrical equipment. The total CapEx bill here typically ranges from $10MM to $13MM per MW, so for 100MW, the data center provider would invest $1B to $1.3B of capital.

CoreWeave is responsible for purchasing the GPUs (Note: As detailed below, CoreWeave does not procure GPUs until after signing its own cloud customer contract).

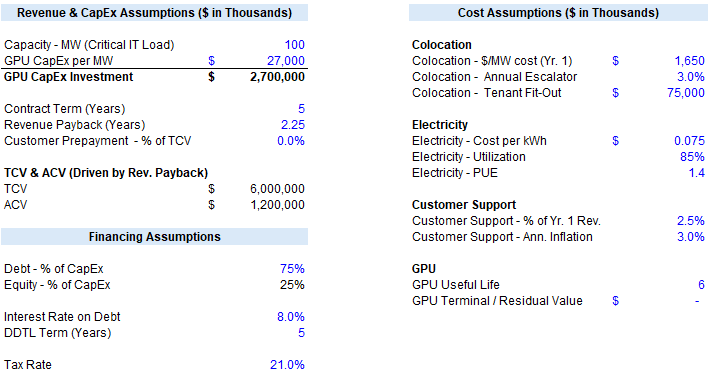

The 100MW Model assumes the following with respect to CoreWeave’s data center lease:

Year-1 rent of $1.65MM per MW, so $165MM for 100MW

3% annual escalator

Tenant fit-out services: $75MM one-time expense in Year-1

Electricity costs are passed through to the tenant (CoreWeave). The 100MW Model assumes: (i) $0.075 per kWh (ii) GPUs run at 85% utilization (iii) the data center operates at a 1.4 PUE (Power Usage Effectiveness)

Now armed with available data center capacity, CoreWeave executes a cloud agreement with its own end-customer. These contracts represent long-term (typically 5+ year) agreements whereby the customer pays for compute from a specific chip architecture. The actual GPUs remain unchanged throughout the 5+ year contract term. For example, a customer signing a contract for GB300s today would still be paying for GB300s in 2030. Given CoreWeave can forecast its major cash outlays (CapEx, data center rent) with a high degree of certainty, it can price its contracts such to achieve a desired IRR. In other words, if CoreWeave is targeting an unlevered IRR of 20%, it can accurately estimate the revenue required to meet this threshold and price the contract accordingly because its expenditures are largely known and fixed. In the 100MW Model, the key terms of the customer contract are:

5 - year term

2.25 year desired revenue payback period, which results in:

$6B total contract value (”TCV”)

$1.2B annual contract value (”ACV”)

CoreWeave then procures GPUs required to service the contract. The 100MW model assumes capital expenditure of $27MM per MW, or $2.7B total, on GPUs (including auxiliary equipment such as networking etc.).

To finance the $2.7B of GPU-CapEx, CoreWeave draws on its Delayed Draw Term Loan (”DDTL”). CoreWeave’s primary credit facilities are structured as DDTLs, which represent commitments by lenders to fund future loans as the borrower (CoreWeave) requires capital. The 100MW Model assumes:

75% of the total $2.7B CapEx outlay is debt-financed, resulting in a $2.0B DDTL draw

The DDTL is priced at S+4.00% (~8% all-in interest rate). Note: In 2024, CoreWeave first DDTL was priced at S + 9.62%. Most recently in July 2025, CoreWeave closed on a $2.6B DDTL commitment at S + 4.00%.

The remaining 25% ($675MM) of the total GPU purchase price is equity-financed with cash on hand.

To reiterate a key point on the lifecycle of a customer contract – CoreWeave only procures GPUs and takes on debt when it has a fully executed customer contract to service.

To be clear, this drastically oversimplifies the process of standing up a GPU cluster, which is an exercise in coordination across construction, engineering, supply management, legal, financial, etc. Building large GPU clusters and operating them is extremely difficult – Semi-Analysis is the go-to resource for learning more about how CoreWeave differentiates here.

100MW Model Assumptions

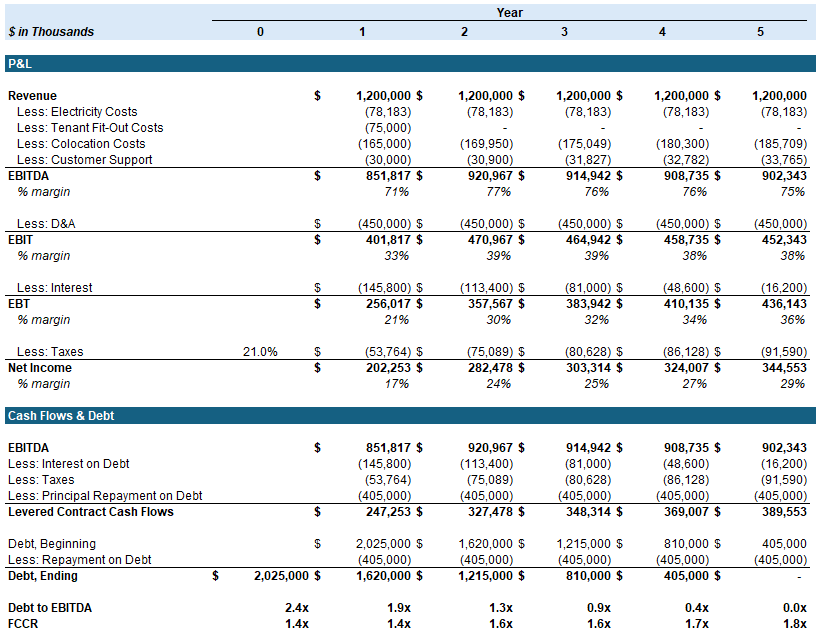

100MW Model Output

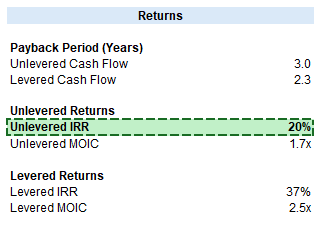

100MW Model Returns

As shown above, the unlevered IRR on the contract is 20%. A few items worth highlighting are noted below, while the Appendix contains additional commentary around the assumptions used.

· Revenue payback is the most important assumption given it drives TCV and ACV (as a function of the assumed CapEx investment)

· There is zero assumed residual value for the GPUs after the 5-year contract.

· Contract-level leverage declines from 2.4x at the onset to zero by Year 5 as the debt is fully amortizing. Even at Year 1, leverage remains modest with fixed charge coverage (EBITDA / Interest + Taxes + Debt repayment) well above 1x.

Margin Profile

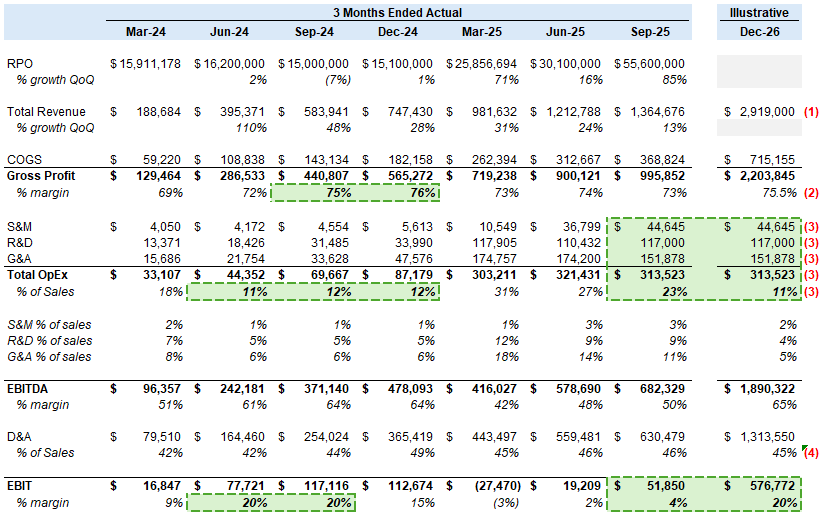

For the quarter ended September 2025, CoreWeave’s reported EBIT margin was 4%, as S&M, R&D, and G&A (“OpEx”) collectively represented 23% of revenue. With contract-level EBIT margins in the ~35% ballpark, there is a clear path for CoreWeave to print 20%+ reported EBIT margins via the realization of operating leverage. For illustrative purposes, we can use the assumptions outlined below to forecast Q4 2026E financials to easily conceptualize the potential for margin expansion:

1. Revenue increases to $2.9B, which is calculated as total revenue backlog of $55.6B, multiplied by 42%, and then divided by 8 (as CoreWeave’s disclosure on backlog states 42% is expected to be recognized in revenue in the next 8 quarters).

2. Gross margins expand modestly to 75.5% (in line with historical levels from Sep. and Dec. 2024, and the Years 2-5 average in the 100MW Model).

3. OpEx is held flat on a dollar basis with Sep. 2025. While I expect CoreWeave to continue to invest in S&M and R&D, this assumption is reasonable given the revenue we are forecasting has already been booked – CoreWeave doesn’t need to make huge investments in R&D and S&M to achieve it. Further, OpEx has been essentially flat over the last 3 quarters (despite significant revenue growth), with stock-based compensation declining following the Q1 2025 IPO.

4. Depreciation and amortization is set to 45% of revenue, roughly in line with Q3 2025 (46%), and consistent with the quarterly average over the last 2 years.

These illustrative assumptions result in an EBIT margin of 20%, with OpEx declining to 11% of revenue from 23% in Sep. 2025. As highlighted above, CoreWeave has already reported 2 quarters of 20% EBIT margin in June and September of 2024.

Other neoclouds’ commentary supports the view that a 20% EBIT margin is realistic for CoreWeave. Nebius has guided towards a medium-term EBIT margin outlook of 20-30%+, while Oracle has pointed to 35% margins for OCI’s AI business. Beyond the realization of operating leverage and economies of scale, additional margin expansion should be driven by the following factors:

· Gross margins are temporarily depressed at the onset of a new contract given the upfront tenant fit-out costs. Over the longer term, as new contract revenue becomes a smaller percentage of total revenue, gross margins should increase.

· Co-location costs as a percentage of revenue should decline as CoreWeave’s previously executed data center leases begin to ramp this year. Through 2024 and 2025, CoreWeave negotiated “bulk discounts” by taking ever larger capacity blocks from Bitcoin miners. For example, CoreWeave’s 590MW lease with Core Scientific (“CORZ”) (est. all-in rate of $1.4MM/MW) is slated to ramp from <20MW as of mid-2025 to 590MW by mid-2027. This lease alone reflects more future capacity than all CoreWeave’s active capacity as of Sep. 2025 and is likely at a significantly lower rental rate versus CoreWeave’s existing leases.

· CoreWeave’s introduction of on-demand compute capacity should be margin accretive. In September 2025, CoreWeave announced a unique arrangement whereby Nvidia would purchase up to $6.3B of any unsold cloud capacity from CoreWeave. This backstop allows CoreWeave to “speculatively” purchase GPUs to offer on-demand (e.g. pay by the hour) capacity to nascent AI start-ups. The on-demand end of the market (which CoreWeave has historically avoided – 98% of current revenue is from long-term contracts) is significantly higher margin as $ per GPU hour on-demand rental rates are well above those for 5-year contractual commitments.

· CoreWeave is evolving its product suite from simply bare-metal GPU compute to include a variety of high-margin software offerings via acquisition. For example, in May 2025, CoreWeave closed the acquisition of Weights & Biases, a provider of machine learnings operations software (e.g. helps AI model developers manage their models) for $1B. In September and October 2025, CoreWeave acquired OpenPipe, Marimo, and Monolith AI. These acquisitions have resulted in near-term margin compression given they are almost certainly not EBITDA positive today, but over time should generate traditional SaaS type revenue.

· CoreWeave’s storage software product (built organically) recently eclipsed $100MM of ARR. In addition, CoreWeave has developed multiple tools (SUNK, or Slurm on Kubernetes and Mission Control) that NVIDIA intends to include within its reference architecture going forward, potentially leading to incremental high margin licensing revenue. Even without selling these products on a standalone basis, CoreWeave can raise prices on its core cloud product as the software solutions result in a stickier, more embedded offering.

· If CoreWeave successfully diversifies its customer base away from large hyperscalers and AI labs and towards enterprises with less technical know-how, its pricing power (and margins) should increase.

· CoreWeave’s stock-based compensation is likely currently elevated relative to go-forward levels given the recency of its IPO and rapid ramp in employee headcount.

Risks

Competitive Dynamics: The main risk to CoreWeave’s business is that its historical growth has been largely driven by a concentrated set of hyperscaler customers, who are also competitors. Furthermore, other customers such as OpenAI intend to eventually build their own data centers, reducing the need for a cloud provider like CoreWeave. In the near-term, this risk is mitigated by CoreWeave’s close relationship with Nvidia. Nvidia provides CoreWeave with early allocations of its latest chip generations, allowing CoreWeave to secure long-term cloud contracts as the largest users of Nvidia’s GPUs (hyperscalers and OpenAI) want access to them as soon as possible. In the medium to longer term, CoreWeave will need to diversify its customer base to the less-sophisticated enterprise customers who lack the resources to stand up large GPU clusters and require a cloud provider like CoreWeave.

OpenAI Concentration: While ~60% of CoreWeave’s revenue backlog comes from investment-grade counterparties (i.e. MSFT META NVDA GOOG), OpenAI represents ~40%. I don’t need to beat a dead horse by stating the obvious: OpenAI has many large cloud commitments and is burning a lot of cash. This exposure is mitigated in a few ways. First, as CoreWeave further diversifies its customer base, exposure to any large customer will decline naturally. CoreWeave’s mgmt. has specifically mentioned that they manage exposure to less creditworthy customers by keeping the overall share of non-investment grade customers in check relative to IG counterparties. Second, given CoreWeave’s (and OpenAI’s) importance to Nvidia, I believe if OpenAI is running low on cash to pay their CoreWeave cloud bills, Nvidia would provide financial support. Finally, if OpenAI is eventually overtaken by Anthropic or Gemini, the capacity CoreWeave built for OpenAI could be easily repurposed to serve either. As an aside, OpenAI’s rapid revenue growth suggests to me the risk of non-payment is overblown, but that’s a topic for another day.

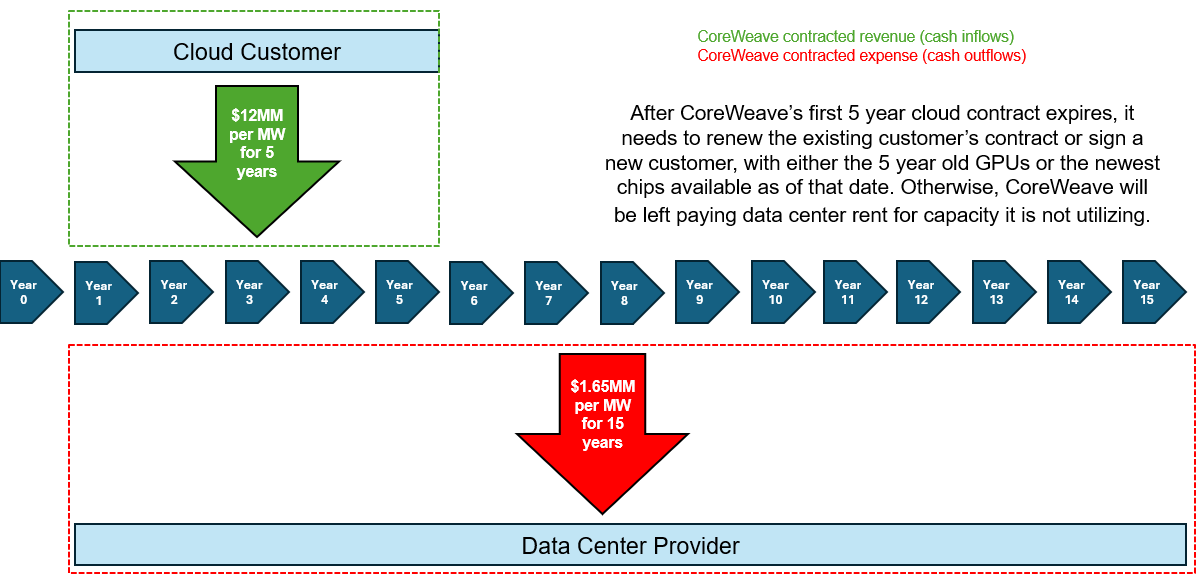

Asset / Liability Mismatch (Renewal Risk): CoreWeave’s customer contracts typically include 5-7 year terms, while its data center leases run for 10-15 years. Thus in 5 to 7 years, CoreWeave will need to renew expiring cloud contracts and / or sign-up new customers or otherwise be left holding the bag (an obligation to rent a data center capacity it isn’t using). Given the nascency and dynamism of the AI cloud business, it remains to be seen how the renewal cycle plays out. That said, early signs are promising, with CoreWeave stating that customers are re-leasing capacity from old chips at rates close to those of the original contract. Furthermore, assuming CoreWeave’s relationship with Nvidia is still strong in 5 years, CoreWeave should still receive priority allocations of Nvidia’s newest chips at that time.

Execution Risk: While CoreWeave continues to prove itself as highly capable of standing up large GPU clusters, execution risk around these complex buildouts remains. On their Q3-2025 earnings call, CoreWeave cut their Q4-2025 revenue and earnings forecast given delays at one of their data centers. While CoreWeave was able to push back the start of delivery of their own cloud services to the customer for which this cluster was built without any adverse impact, future delays could lead to contract cancellations. CoreWeave has mitigated the execution risks associated with its data center developers failing to deliver on time by diversifying their base of data center providers and starting their own self-builds. It should also be noted that the interest rate on CoreWeave’s DDTLs have declined from S + 9.62% to S + 4.00% over the last 18 months. A portion of this decline reflects CoreWeave demonstrating themselves as highly capable operators who execute on their customer contracts.

Reliance on NVIDIA: CoreWeave is heavily dependent on NVIDIA, and any disruption to their relationship would be catastrophic. NVIDIA’s early allocations of new GPUs are crucial in allowing CoreWeave to secure large, long-term commitments from the world’s largest technology companies. Without these early allocations, I highly doubt CoreWeave would currently stand at $5B+ of annualized revenue and $56B of revenue backlog. Fortunately for CoreWeave, the bet made in 2022 to go all-in on NVIDIA GPUs and build an AI cloud platform has paid off, as Jensen quite clearly favors them. Their strategic importance to NVIDIA seems to be ever-increasing as Google and Amazon ramp their production of in-house GPU alternatives... just look at NVIDIA’s $2.0B investment in CRWV shares last month. While CoreWeave and NVIDIA appear to be growing more closely aligned, it’s worth acknowledging that CoreWeave is reliant on NVIDIA and monitoring this relationship accordingly.

Summary Conclusions

CoreWeave’s unit-economics are quite attractive, with estimated contract-level unlevered IRRs at ~20%.

These returns are NOT dependent upon GPU residual values or the re-contracting of old GPUs following a contract’s expiration, which represent upside to the estimated 20% unlevered IRR.

CoreWeave’s current reported EBIT margin is temporarily depressed given recent S&M, R&D, and G&A investments. As disclosed in its S-1, CoreWeave’s EBIT margin was actually 20% in June and September 2024 prior to a significant ramp in OpEx ahead of its March 2025 IPO.

Over time, as the business continues to scale (CoreWeave’s revenue backlog of $55.6B implies 2026E revenue will be more than double 2025E) and realize operating leverage, I expect EBIT margins north of 20%.

· CoreWeave’s use of debt is appropriate given its GPUs are servicing 5+ year, highly financeable, contracted revenue streams. CoreWeave is NOT issuing debt to speculatively purchase GPUs in the hopes of later finding customers.

CoreWeave’s DDTL facilities fully amortize within the term of its customer contracts. This structure provides strong protection to its lenders as each contract naturally deleverages over time.

CoreWeave’s consolidated leverage fluctuates based on the degree to which it is drawing on its DDTL to execute new contracts, as leverage peaks at a contract’s onset.

CoreWeave’s lenders are the real arbiter of its credit profile given they are the entities with their capital at-risk. The fact they went from pricing its debt at S + 9.62% in 2024 to S + 4.00% most recently is a clear signal that CoreWeave’s credit profile is improving.

CoreWeave’s use of debt allows it to scale significantly faster than otherwise. Assuming 75% debt, 25% equity funding for GPU CapEx, CoreWeave can take $1 of equity and buy $4 of GPUs, which has enabled its rapid growth and emergence as a legitimate competitor to the traditional hyperscalers.

The main risk to CoreWeave is that its historical growth and existing backlog is driven by a concentrated set of hyperscaler customers, who are also competitors. CoreWeave’s close relationship with Nvidia helps to mitigate this risk.

The risk that CoreWeave defaults on its obligations to its data center landords are overblown, and an immediate rent default (within next 5 years) seems extremely unlikely. However, the asset / liability timing mismatch poses risks over the medium to longer term. If CoreWeave’s own customers do not renew in 5-7 years when their contracts expire and CoreWeave cannot replace them, CoreWeave will be paying for data center capacity they aren’t using. Early signs are positive, as CoreWeave has renewed expiring contracts on attractive terms. Furthermore, the increasingly longer contract durations on recent deals helps mitigate this risk. Finally, CoreWeave priority allocations of NVIDIA’s latest chips help increase the odds it can find contracts for its data center capacity as it becomes available.

GPU useful life is NOT a risk for CoreWeave’s debt or equity holders and largely represents potential upside for shareholders.

CoreWeave’s long-term success depends on its ability to diversify its customer base away from hyperscalers and AI labs and towards enterprises who possess less in-house technical expertise and are more likely to rely upon an outsourced AI cloud provider like CoreWeave. While enterprise adoption of GPU-cloud services is nascent, the longer-term market opportunity is likely massive (for example, Nebius has commented that they believe 2/3 of the market is from enterprises).

CoreWeave should also continue to differentiate by embedding higher-margin software tools within their cloud offering.

Appendix

Assumptions

GPU CapEx per MW: $27MM is in-line with Sep. 2025 balance sheet & MW disclosures.

Note: Jensen also stated on Nvidia’s latest earnings call that with respect to NVIDIA content per gigawatt, “Grace Blackwell is probably $30 billion”, suggesting $27MM per MW is reasonable.

Contract Term: While CoreWeave’s S-1 disclosed a weighted-average contract duration of approximately four years as of Dec. 2024, contract lengths observed for both CoreWeave’s deals and other GPU cloud deals (e.g. Nebius) with publicly disclosed details have increased to 5+ years over the course of 2025 and early 2026. For example, as disclosed in an 8-K, CoreWeave’s contract with Meta runs through December 2031 (6 years from signing), with the option to extend to 2032 (7 years). Further, CoreWeave’s disclosure on unsatisfied RPO in its Sep. 2025 10-Q also states that 19% of the $50B RPO balance is expected to be recognized between months 49 and 84 (or 5 to 7 years out). The S-1 disclosure capped the expected recognition of unsatisfied RPO to 6 years.

Revenue (and unlevered CF) Payback: The assumed 2.25 year revenue payback period results in a ~3 year unlevered cash flow payback. While CoreWeave’s S-1 disclosed an anticipated 2.5 year cash payback as of Dec. 2024, our analysis assumes that cash payback periods have elongated to 3 years due to the elongation of contract terms (4 years in the S-1 vs. 5 years in the 100MW Model). Said differently, CoreWeave is OK with longer payback periods given the contract itself is longer.

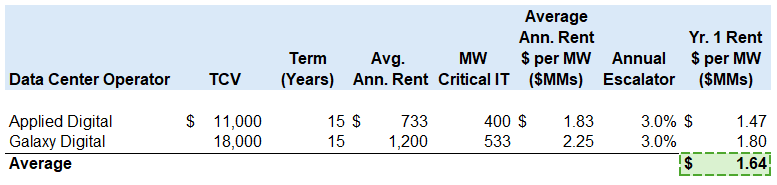

Colocation ($/MW, Tenant Fit-Out): $1.65MM/MW approximates the average starting base rent for CoreWeave’s leases with Applied Digital and Galaxy:

The Tenant Fit-Out Assumption of $75MM was based on Applied Digital’s latest 10-Q, which stated they “earned approximately $73MM for tenant fit-out services during the current quarter”. Applied Digital fully energized their first 100MW building for CoreWeave during this quarter, making the $73MM figure a reasonable estimate for the purposes of our 100MW analysis.

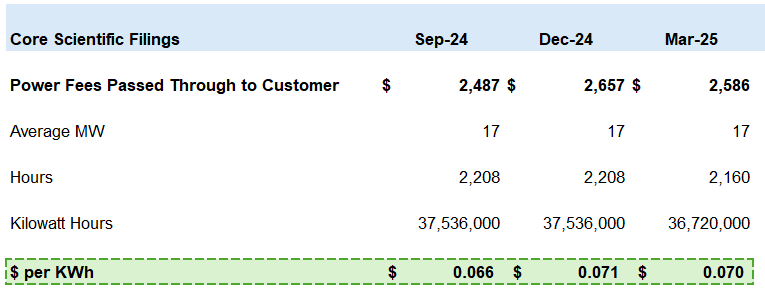

Electricity: Per Core Scientific (CORZ)’s 10-Qs, CoreWeave is paying $0.066 to $0.071 per KWh. Note only Sep. 2024 – March 2025 are shown below as these are the only quarters whereby CORZ disclosed the total MW energized for its lease with CoreWeave:

Our analysis assumes a higher power price to reflect the ongoing increases in broader power prices.

Debt (% of CapEx Debt Funded, Interest Rate): Our assumption of 75% of CapEx debt-funded is based on the following:

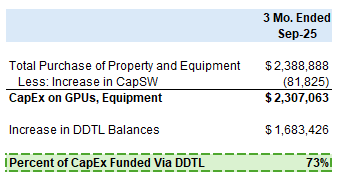

From CoreWeave’s Sep. 2025 10-Q, we can estimate 73% of their CapEx was funded via DDTL draw:

CoreWeave’s principal debt balance of $14.2MM as of Sep. 2025 vs. $3.9B book value of equity implies 79% debt to total capital.

Our 8% assumed interest rate is based on the SOFR + 4.00% rate of CoreWeave’s most recent DDTL issuance (DDTL 3.0):

NWC impacts were not considered to be material for the purposes of this analysis. Note also that CoreWeave’s DPOs are greater than DSOs, implying potential NWC cash flow benefits.

Cash taxes were assumed to be 21% of pre-tax income, with straight-line depreciation (conservatively modeled given OBBB allows for 100% bonus depreciation).

Other Additional Commentary

The $12MM/MW in revenue shown herein is modestly above the ~$10MM/MW in deals announced by other neoclouds. This “premium” reflects that (i) CoreWeave is known to have higher pricing than other neoclouds due to their ability to lower the TCO for their customers and (ii) the 100MW model does not assume any customer prepayment, which all else equal results in a lower revenue figure (i.e. the cloud provider accepts a lower TCV/ACV in exchange for the customer paying a portion of the TCV upfront). In addition, in the 9 months September 2025 YTD, CoreWeave has added $2.5B of net new annualized run-rate revenue and 230MW of active power, implying $10.7MM rev. / MW for capacity added in 2025. This is well north of the $8.3MM rev. / MW as of Dec. 2024, suggesting recent deals are generating more revenue per MW. To summarize, based on publicly available information, trends in CoreWeave’s financials, and industry chatter around CoreWeave’s pricing, the $12MM/MW in revenue appears reasonable.

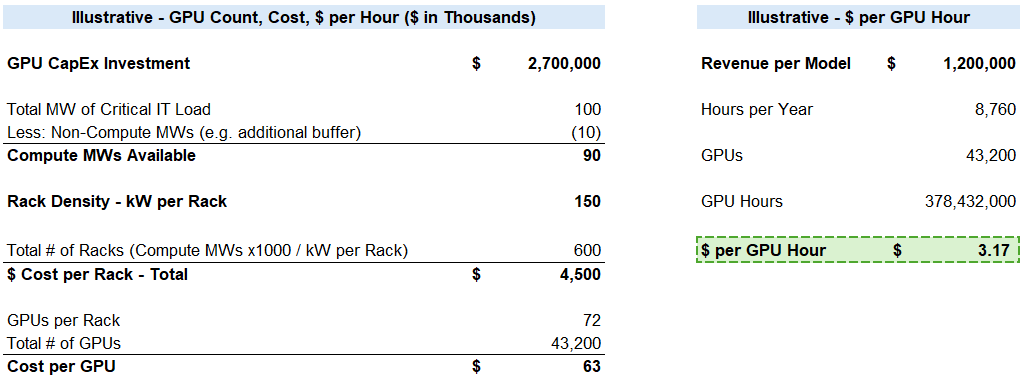

To further stress test the concluded $12MM/MW in revenue, if we assume 150kW rack density and 10 in non-compute MWs, we can deduce that $2.7B in GPU-related CapEx buys 600 racks and 43,200 GPUs (given each rack = 72 GPUs). At $1.2B rev. and 100MW (e.g. $12MM/MW), the implied $ per GPU Hour is $3.17, which is reasonable relative to competitors’ public pricing on Grace Blackwell rentals.

Lastly, the 100MW Model uses TCV and contract length (as a function of payback period on CapEx) to derive annual revenue. Another way to model revenue is at the GPU level (e.g. total CapEx investment is = # of GPUs x Price per GPU and revenue is = # of GPUs x Rev $ per GPU Hour). The issue here is that both Nvidia and CoreWeave are unsurprisingly coy on what a GPU actually costs and what discounts CoreWeave may or may not receive given their strategic importance to Nvidia. My main takeaway from this exercise is that because CoreWeave can accurately estimate their expenditures, they are able to pencil in their returns, which are attractive based on all available evidence.